Top 10 Best Books On Econometrics

Economics is a distinct subject. However, you won't be able to use the concepts effectively unless you learn the mathematical and statistical aspects of the ... read more...subject thoroughly. And herein lies the significance of econometrics. The following is a list of the best books on economometrics.

-

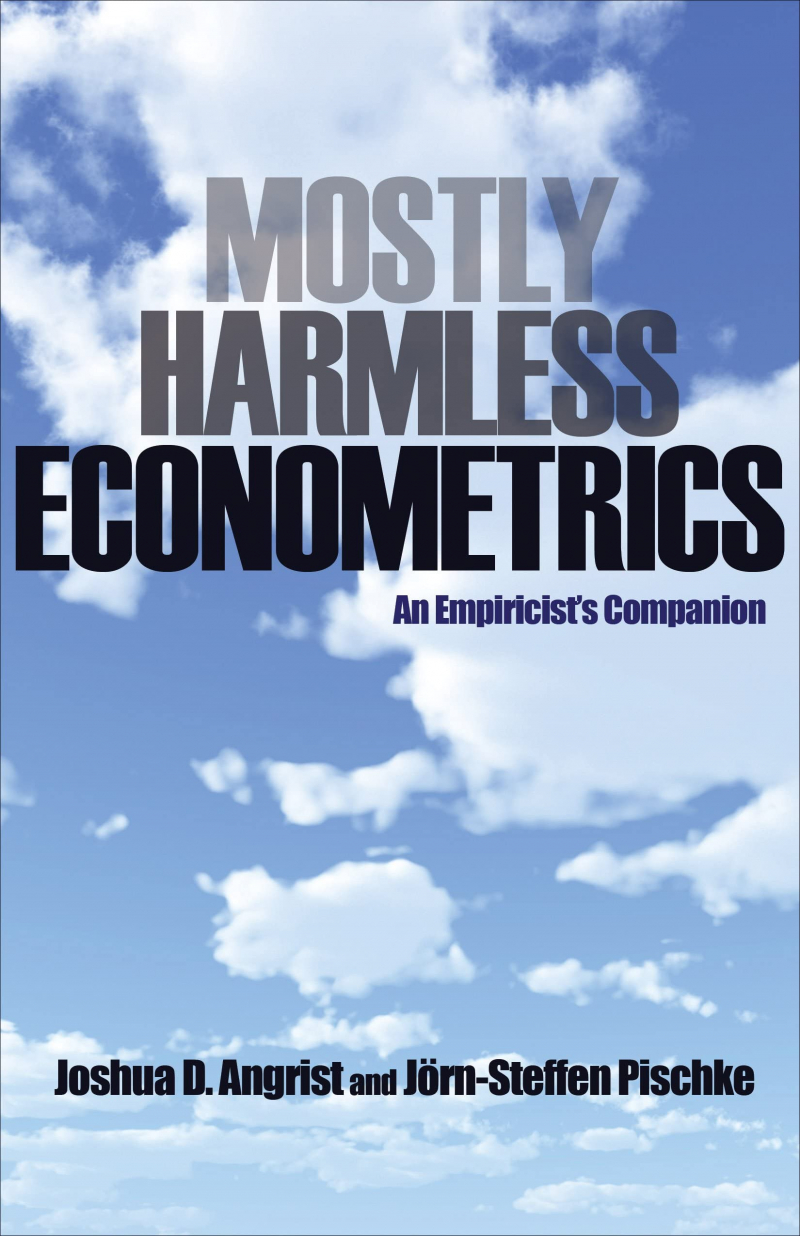

Joshua D. Angrist is the Ford Professor of Economics at the Massachusetts Institute of Technology and the winner of the 2021 Nobel Prize in Economics. Professor Jörn-Steffen Pischke teaches economics at the London School of Economics and Political Science.

Linear regression for statistical control, instrumental variables methods for natural experiment analysis, and differences-in-differences methods that exploit policy changes are the core methods in today's econometric toolkit. These techniques, according to the modern experimentalist paradigm, address clear causal questions such as: Do smaller classes increase learning? Should husbands who batter their wives be arrested? How much does education increase pay? Mostly Harmless Econometrics demonstrates how the fundamental tools of applied econometrics allow the data to speak for itself.

Mostly Harmless Econometrics covers important new extensions such as regression-discontinuity designs and quantile regression, as well as how to get standard errors right. Fancier econometric techniques, according to Joshua Angrist and Jörn-Steffen Pischke, are usually unnecessary and even dangerous. The applied econometric methods emphasized in this book are simple to apply and applicable to a wide range of contemporary social science fields.

- An irreverent look at the fundamentals of economics

- a focus on the tools most commonly used by applied researchers

- Regression-discontinuity designs, quantile regression, and standard errors are all covered in detail.

- There are numerous empirical examples.

- A concise and useful resource with numerous applications.

Author: Joshua David Angrist and Jörn-Steffen Pischke

Link to buy: https://www.amazon.com/dp/0691120358

Ratings: 4.7 out of 5 stars (from 478 reviews)

Best Sellers Rank: #90,289 in Books

#9 in Econometrics & Statistics

#16 in Economics (Books)

https://www.amazon.com/

https://www.amazon.com/ -

This Econometrics book is a straightforward, simple, and easy-to-understand introduction to econometrics. If you're a student who knows nothing about econometrics, this best Econometrics book is a great place to start. You don't have to know everything, but if you read a few chapters of this book and understand the basics of regression analysis, you'll be fine. Econometrics is not for the faint of heart. But that doesn't mean it can't be explained in an understandable way.

This Econometrics book demonstrates that econometrics can be beautifully explained without the use of unnecessary words or phrases.Among the best books on economometrics, Using Econometrics is intended for those who want to learn the fundamentals of econometrics. So, if you're looking for an econometrics book for your Ph.D. studies, this isn't it. But, yes, you can easily start with this book, understand regression analyses thoroughly, and then move on to a more dense and intense econometrics book. You'll get simple explanations for each topic and be able to connect your knowledge to the stunning visuals in this book. In a nutshell, this is an excellent primer for beginning your econometrics journey.

- This best-selling Econometrics book is written for beginners and has done a good job over the last 30 years.

- The focus of this book is "single-equation linear regression analysis." Real-life examples make it very easy to understand the concepts.

Author: A. Studenmund

Link to buy: https://www.amazon.com/gp/aw/d/013418274X/

Ratings: 4.5 out of 5 stars (from 173 reviews)

Best Sellers Rank: #826,381 in Books

#121 in Econometrics & Statistics

#842 in Economics (Books)

https://fr.scribd.com/

https://fr.scribd.com/ -

If you're looking for an Econometrics book to help you in class, look no further. As the title suggests, it is an excellent starting point for anyone interested in econometrics. Furthermore, if you purchase this best Econometrics book, you will not need to seek assistance from instructors or teachers. You can study independently and pass the exam. Introduction to Econometrics may not be useful if you are new to economics. It is only useful for those working on applied econometrics or considering doing so. There are no parallels between traditional textbooks. No, this book is unique. It will show you how econometrics can help you get past ambiguity and find answers to pressing questions. This guide will show you how to present data in R, Stata, Microsoft Excel, Minitab, EViews, and Text. You will also learn how to apply actual practices and challenges in today's business world, as well as the relevance of econometrics in real life.

- You will also receive MindTap technology, which will assist you in mastering the subject through interactive materials and animation videos, in addition to this Econometrics book.

- Even though it is a beginner's guide, this top Econometrics textbook is quite comprehensive (more than 780 pages of materials). It is one of the best textbooks for students to use when studying for econometrics exams.

Author: James H. Stock and Mark Watson

Link to buy: https://www.amazon.com/gp/aw/d/0134461991/

Ratings: 4.3 out of 5 stars (from 42 reviews)

Best Sellers Rank: #698,252 in Books

#105 in Econometrics & Statistics

#651 in Economics (Books)

Amazon.ca

Amazon.ca -

Jeffrey M. Wooldridge has been a University Distinguished Professor of Economics at Michigan State University since 1991. Dr. Wooldridge received his B.A. from the University of California, Berkeley, with majors in computer science and economics, and his Ph.D. in economics from the University of California, San Diego.

This acclaimed graduate text's second edition provides a unified treatment of two methods used in contemporary econometric research, cross section and data panel methods. The book maintains an appropriate level of rigor while emphasizing intuitive thinking by focusing on assumptions that can be given behavioral content. The analysis includes models with dynamics and/or individual heterogeneity, as well as linear and nonlinear models. Specific linear and nonlinear methods are covered in detail, including probit and logit models and their multivariate, Tobit models, models for count data, censored and missing data schemes, causal (or treatment) effects, and duration analysis, in addition to general estimation frameworks (particular methods of moments and maximum likelihood).

The first graduate econometrics text, Econometric Analysis of Cross Section and Panel Data, focused on microeconomic data structures, allowing assumptions to be separated into population and sampling assumptions. This second edition has been updated and revised extensively. Improvements include a broader class of models for missing data problems, a more detailed treatment of cluster problems, an important topic for empirical researchers, an expanded discussion of "generalized instrumental variables" (GIV) estimation, new coverage of inverse probability weighting (based on the author's own recent research), a more complete framework for estimating treatment effects with panel data, and a firmly established link between econometric approaches to n New emphasis is placed on explaining when specific econometric methods can be used; the goal is not only to tell readers what works, but also why certain "obvious" procedures do not. The numerous exercises included, both theoretical and computer-based, allow the reader to extend methods covered in the text and gain new insights.

Author: Jeffrey M. Wooldridge

Link to buy: https://www.amazon.com/dp/0262232588

Ratings: 4.5 out of 5 stars (from 119 reviews)

Best Sellers Rank: #533,180 in Books

#68 in Econometrics & Statistics

#392 in International Economics (Books)

#442 in Economics (Books)

https://www.amazon.com/

https://www.amazon.com/ -

Peter Kennedy is an economist at Simon Fraser University. He is the author of Macroeconomic Essentials: Understanding Economics in the News, 2e (2000), as well as A Guide to Econometrics, and an Associate Editor of the International Journal of Forecasting, the Journal of Economic Education, and Economics Bulletin.

This is a must-have reference book for any Econometrics class. No. It should be used for more than just a textbook on econometrics. However, it is an excellent supplement when a textbook is available. Consider having a personal tutor sitting with you all day to teach you the intricacies of econometrics. A Guide to Econometrics is of such high quality that you will frequently feel that way. Many econometrics textbooks discuss broad theories while expecting you to understand specific models. But this book is unique. The author skips over general theories and goes straight to the point in plain English. This method is far superior because many students must learn about the subject for the first time when they begin studying econometrics. Many readers recommend skipping Greene and Wooldridge and instead reading this book before econometrics becomes a source of frustration. The author also ensures that the students understand the equations and theory language in this book, so rote memorization is not required. Furthermore, there is no jargon, different words, or extraneous phrases. Kennedy outperforms the other authors of Econometrics.

- This book on Econometrics is very easy to read, and it contains the most up-to-date information on instrumental variables and computational considerations.

- This book contains numerous examples as well as useful formulas. You will also learn about GMM, nonparametric statistics, and wavelets.

Author: Peter Kennedy

Link to buy: https://www.amazon.com/dp/1405182571

Ratings: 4.6 out of 5 stars (from 104 reviews)

Best Sellers Rank: #1,019,389 in Books

#165 in Econometrics & Statistics

#1,177 in Economics (Books)

https://www.amazon.com/

https://www.amazon.com/ -

Roberto Pedace, PhD, is an associate professor in Scripps College's Department of Economics. His work has appeared in journals such as Economic Inquiry, Industrial Relations, the Southern Economic Journal, Contemporary Economic Policy, and the Journal of Sports Economics, among others.

Econometrics can be difficult for many students who are unfamiliar with the terms and concepts covered in a typical econometrics course. Econometrics For Dummies clears up the confusion by providing simple explanations of important economic topics.

Econometrics For Dummies simplifies this complex subject and offers an easy-to-follow course supplement to help you further refine your understanding of how econometrics works and how it can be applied in real-world situations. It is regarded as one of the best books on economometrics.

- A fantastic resource for anyone taking a college or graduate level econometrics course.

- Gives you a simple introduction to the techniques and applications of econometrics.

- Assists you in achieving a high exam score

If you're studying economics and want a simple guide to this often-confusing subject, Econometrics For Dummies is the book for you. It is regarded as one of the best books on econometrics.

Author: Roberto Pedace

Link to buy: https://www.amazon.com/dp/1118533844

Ratings: 4.4 out of 5 stars (from 170 reviews)

Best Sellers Rank: #335,070 in Books

#39 in Econometrics & Statistics

https://www.amazon.com/

https://www.amazon.com/ -

Bruce E. Hansen is one of the world's most cited econometricians and the Mary Claire Aschenbrener Phipps Distinguished Chair of Economics at the University of Wisconsin-Madison.

Econometrics is the quantitative language of economic theory, analysis, and empirical research, and it has become a foundational component of graduate economics programs. Econometrics is an essential introduction to this foundational subject in economics for graduate and PhD students, as well as an invaluable reference for researchers and practitioners. This comprehensive textbook covers fundamental concepts, focuses on modern, real-world applications, and provides students with an intuitive understanding of econometrics.

- Covers the entire range of econometric theory and methods with mathematical rigor, with an emphasis on intuitive explanations that are understandable to students of all backgrounds.

- Uses integrated, research-level datasets from an accompanying website.

- Linear econometrics, time series, panel data, nonparametric methods, nonlinear econometric models, and modern machine learning are all covered.

- It contains hundreds of exercises that allow students to learn by doing.

- Includes extensive appendices on matrix algebra and useful inequalities, as well as a plethora of real-world examples.

- Can be used as a core textbook for a first-year PhD econometrics course and as a supplement to Bruce E. Hansen's Probability and Statistics for Economists.

Author: Bruce Hansen

Link to buy: https://www.amazon.com/Econometrics-Bruce-Hansen/dp/0691235899/

Ratings: 5 out of 5 stars (from 8 reviews)

Best Sellers Rank: #149,945 in Books

#14 in Econometrics & Statistics

#39 in Economics (Books)

#62 in Business Encyclopedias

https://www.amazon.com/

https://www.amazon.com/ -

Harvard University's Otto Eckstein Professor of Applied Economics is John Y. Campbell. Andrew W. Lo is a Harris & Harris Group Professor of Finance at the Massachusetts Institute of Technology's Sloan School of Management. A. Craig MacKinlay is the Joseph P. Wargrove Professor of Finance at the University of Pennsylvania's Wharton School.

The use of quantitative methods in financial markets has increased dramatically over the last two decades. In portfolio management, proprietary trading, risk management, financial consulting, and securities regulation, finance professionals now routinely employ sophisticated statistical techniques. This graduate-level textbook is designed for PhD students, advanced MBA students, and industry professionals interested in financial modeling econometrics. The Econometrics of Financial Markets, one of the best books on economometrics, covers the entire range of empirical finance, including asset return predictability, tests of the Random Walk Hypothesis, the microstructure of securities markets, event analysis, the Capital Asset Pricing Model and the Arbitrage Pricing Theory, interest rate term structure, dynamic models of economic equilibrium, and nonlinear financial models such as ARCH, neural networks, statistical fractals, and chaos theory.

Each chapter focuses on statistical techniques in the context of a specific financial application. This exciting new text offers a unique and approachable blend of theory and practice, bringing cutting-edge statistical techniques to the forefront of financial applications. Each chapter also includes a discussion of recent empirical evidence, such as the rejection of the Random Walk Hypothesis, as well as problems designed to help readers apply what they've learned.

Author: A. Craig MacKinlay, Andrew W. Lo and John Y. Campbell

Link to buy: https://www.amazon.com/Econometrics-Financial-Markets-John-Campbell/dp/0691043019/

Ratings: 4.6 out of 5 stars (from 62 reviews)

Best Sellers Rank: #189,350 in Books

#21 in Econometrics & Statistics

#48 in Business Investments

#1,279 in Investing (Books)

https://www.amazon.com/

https://www.amazon.com/ -

At McGill University in Montreal, Russell Davidson holds the Canada Research Chair in Econometrics. He also teaches at GREQAM in Marseille and previously taught at Queen's University for many years. He holds a doctorate in physics from the University of Glasgow and a doctorate in economics from the University of British Columbia.

James G. MacKinnon is the Sir Edward Peacock Professor of Econometrics and Head of the Department at Queen's University in Kingston, Ontario, Canada, where he has taught since 1975, when he received his Ph.D. from Princeton.

Econometric Theory and Methods is a comprehensive treatment of modern econometric theory and methods. The geometrical approach to least squares, as well as the method of moments, which is used to motivate a wide range of estimators and tests, are emphasized. Simulation methods, such as the bootstrap, are introduced early and widely used.

The book covers a wide range of contemporary topics. Sandwich covariance matrix estimators, artificial regressions, estimating functions and the generalized method of moments, indirect inference, and kernel estimation are among the others. Every chapter includes a variety of exercises, some theoretical, some empirical, and many of which involve simulation.

Econometric Theory and Methods is intended for first-year graduate courses. The book is appropriate for both one-term and two-term Masters or Ph.D. courses. It can also be used in a final-year undergraduate course for students with sufficient mathematical and statistical backgrounds. It is among the best books on economometrics.

Author: Russell Davidson and James G. MacKinnon

Link to buy: https://www.amazon.com/Econometric-Theory-Methods-Russell-Davidson/dp/0195123727/

Ratings: 4.8 out of 5 stars (from 24 reviews)

Best Sellers Rank: #208,464 in Books

#6 in Economic Theory (Books)

#22 in Econometrics & Statistics

#186 in Theory of Economics

https://www.amazon.com/

https://www.amazon.com/ -

A. Colin Cameron is an Economics Professor at the University of California, Davis. He is currently the Director of the Center for Quantitative Social Science Research at that university. He has also taught at Ohio State University and held visiting positions at Indiana University at Bloomington, as well as a number of Australian and European universities.

Pravin K. Trivedi is the John H. Rudy Professor of Economics at Indiana University. He has also taught at The Australian National University and the University of Southampton, as well as a number of European universities on a short-term basis.

Microeconometrics: Methods and Applications is the most thorough treatment of microeconometrics to date, which is the analysis of individual-level data on the economic behavior of individuals or firms using regression methods for cross section and panel data. The book is written with the practitioner in mind. It is assumed that you have a basic understanding of the linear regression model and matrix algebra. The text is appropriate for a microeconometrics course, typically a second-year economics PhD course; data-oriented applied microeconometrics field courses; and as a reference work for graduate students and applied researchers looking to fill gaps in their toolkit.

The emphasis on nonlinear models and robust inference, simulation-based estimation, and problems with complex survey data are distinguishing features of the book. To illustrate the key models and methods, the book frequently employs numerical examples based on generated data. More importantly, it systematically incorporates empirical illustrations based on seven large and exceptionally rich data sets into the text.

Author: A. Colin Cameron and Pravin K. Trivedi

Link to buy: https://www.amazon.com/Microeconometrics-Methods-Applications-Colin-Cameron/dp/0521848059/

Ratings: 4.5 out of 5 stars (from 54 reviews)

Best Sellers Rank: #274,924 in Books

#33 in Econometrics & Statistics

#48 in Microeconomics (Books)

#291 in Probability & Statistics (Books)

https://www.amazon.com/

https://www.amazon.com/